As corporate profits surge on Wall Street, a growing number of small firms are closing their doors, squeezed by high prices, rising borrowing costs, and the weight of bigger competitors. The contrast is pushing a debate to the forefront: who benefits from the current economy, and who pays the price? A recent panel on The Big Money Show examined the split, asking whether Main Street can survive if current pressures persist.

The discussion comes at a time when credit has grown more expensive, pandemic-era savings have faded, and input costs remain sticky for many owners. While large companies can raise capital more easily and negotiate better terms with suppliers, many small operators face thinning margins and slower foot traffic. Bankruptcies among smaller firms have climbed in recent months, even as several major indexes hover near highs.

Inflation’s Lingering Grip On Main Street

For many independent shops and service providers, higher costs still flow through their books. Rent renewals, insurance premiums, and wholesale prices have not fallen as quickly as hoped. Owners often resist passing full increases to customers, worried about losing business. The gap shows up in cash flow and late payments.

Some firms locked in long-term leases during better times and now face steeper renewal rates. Others rely on inventory that became more expensive when supply chains snarled, and those higher-cost goods are still working through shelves. When sales slow, those items tie up precious capital.

Rising Rates And Tighter Credit

Borrowing has become harder and pricier. Higher interest rates raise monthly payments on lines of credit, equipment loans, and commercial mortgages. Banks have tightened standards after recent stress in regional lenders, leaving fewer options for marginal borrowers.

That change widens the gap between small firms and large corporations. Big companies can tap bond markets and refinance at scale. Smaller operators often depend on a single community bank. When that bank tightens, there may be no fallback.

Corporate Scale And Competitive Pressures

Large retailers and platforms can negotiate lower prices and faster shipping from suppliers. They can also run promotions that smaller rivals cannot match. This scale advantage can pull customers away from local stores, even when those stores offer better service.

Online platforms also set the terms for search visibility and fees, forcing many small sellers to pay more to reach the same customers. When ad costs rise, small margins get thinner.

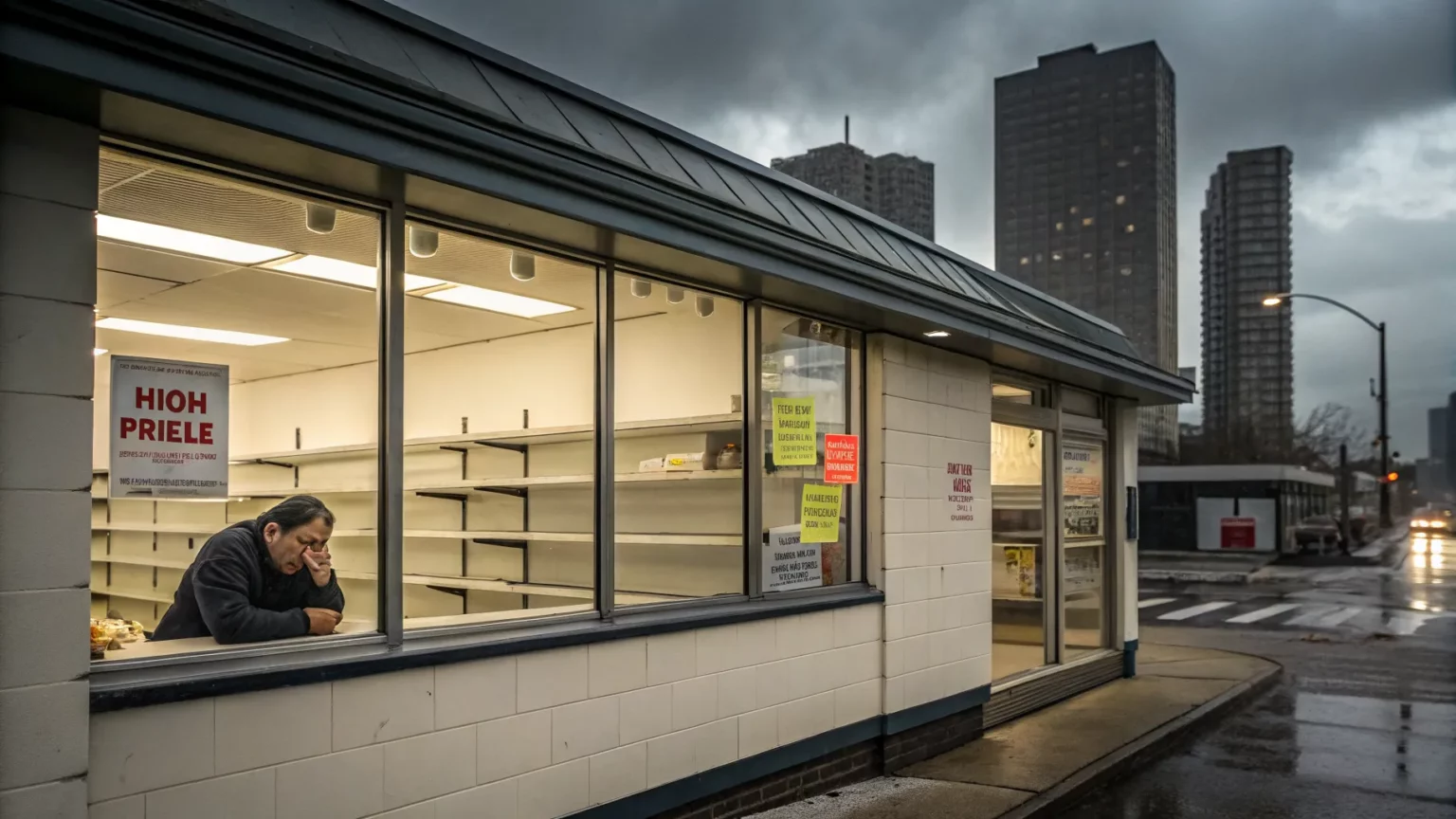

Wall Street’s Highs Versus Main Street’s Lows

The panel framed the split in stark terms, pointing to strong earnings in finance and tech while small-business failures mount. One passage captured the tension:

‘The Big Money Show’ panel discusses whether small businesses are being squeezed by inflation, high borrowing costs and corporate dominance as Wall Street profits soar and bankruptcies on Main Street hit record highs.

The concern is not only fairness. It is also economic health. Small businesses employ millions and anchor local communities. When they falter, hiring slows, storefronts empty, and neighborhoods lose services.

What The Trend Could Mean Next

If rates stay high, more owners may delay expansion, reduce hours, or cut staff. If input costs cool and credit loosens, relief could come through better margins and renewed investment. Policymakers will watch for signs of stress such as rising delinquencies and falling new business formation.

- Watch credit conditions at regional banks and small-business lenders.

- Track commercial rent trends and lease renewals in local corridors.

- Monitor inventory markdowns and discounting by large retailers.

- Follow new business applications and closures as early signals.

Owners Seek Practical Adjustments

Many firms are responding with tighter cost controls, simplified product lines, and careful pricing moves. Some are pooling purchases through co-ops to gain better terms. Others are shifting to services with steadier demand or building direct customer channels to reduce fees.

While these steps help, they may not offset headwinds if consumer demand weakens. The balance between cost discipline and customer retention will be central in the months ahead.

The split between strong market profits and fragile local businesses is drawing sharper focus. The key question is whether easing inflation and steadier credit can arrive soon enough to slow closures on Main Street. For now, many owners remain in a defensive stance, planning for leaner months and hoping for a gentler rate path. The next few quarters will show whether resilience, policy shifts, or renewed demand can turn the tide—or whether more storefronts go dark before relief arrives.